What's Hot: 1,800 Units In The Works: Connecticut Avenue's Building Boom | New EYA Townhomes Just Steps to Metro

A Decline in Class A Apartment Rents on the Horizon?

A Decline in Class A Apartment Rents on the Horizon?

✉️ Want to forward this article? Click here.

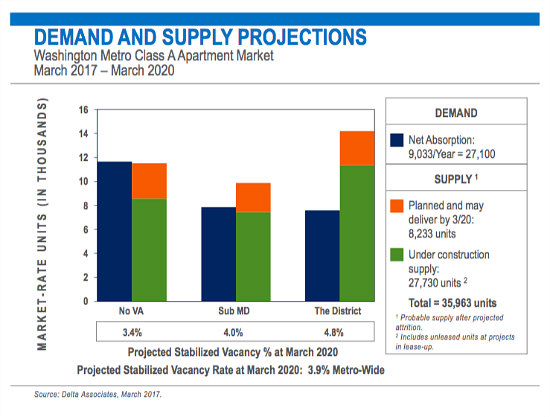

The last time UrbanTurf examined the state of the Class A rental market in the DC region, absorption had dropped for the first time in seven consecutive quarters, seemingly following the predicted trend of a slow-down in area demand.

Now, the most recent report from Delta Associates shows that absorption has rebounded — but that where the District is concerned, the market could still be headed down a path that leads to higher vacancies and lower rents for new apartment product.

story continues below

loading...story continues above

In the region, the pace of absorption has withstood the large number of new projects that have delivered and are leasing up. Specifically, absorption of Class A apartments in the DC area is still well above the 10-year average, with 10,381 units absorbed year-over-year through March 2017. However, in DC proper, two sub-markets seem to epitomize the Class A rental market dynamics.

“While rent growth will likely be muted and vacancy may rise on average across the District due to increased supply over the next couple of years, there are just two submarkets which are mainly driving these dynamics – the Capitol Hill/Riverfront/Southwest and NoMa/H Street submarkets,” explains William Rich, president of Delta Associates. “Over 70% of the projected oncoming supply will be located in these two rapidly growing submarkets. Nevertheless, the impact is District-wide – stabilized vacancy is up over the year in all submarkets and rents declined in all but two of them.”

Rich pointed out that annual absorption fell by more than 50 percent from 2016 in the NoMa/H Street sub-market, but increased by nearly 70 percent in Capitol Hill/Riverfront/SW. “About 40 percent of absorption in the District over the past 12 months came from the Capitol Hill/Riverfront/SW submarket.”

Here is a quick snapshot of average rents for high-rise Class A apartments in DC area sub-markets, as defined by Delta:

Note: The rents are an average of studios, one and two-bedroom rental rates at new buildings in the DC area.

Definitions:

Class A apartments are typically large buildings built after 1991, with full amenity packages. Class B buildings are generally older buildings that have been renovated and/or have more limited amenity packages.

See other articles related to: absorption rate, class a, class a apartments, delta associates, rental rates in dc, renting in dc

This article originally published at http://dc.urbanturf.production.logicbrush.com/articles/blog/a_decline_in_class_a_apartment_rents_on_the_horizon/12438.

UrbanTurf Listings showcases the DC metro area's best properties available for sale.

Most Popular... This Week • Last 30 Days • Ever

The wait for Eataly in the DC area has been a long one.... read »

EYA and the Washington Metropolitan Area Transit Authority have requested a two-year ... read »

While the broader DC-area housing market grapples with elevated mortgage rates and ca... read »

Justice Roberts selling Maryland home; bathroom danger; and what will future stadiums... read »

From the Maryland line down to the edge of downtown, a mix of office conversions, inf... read »

DC Real Estate Guides

Short guides to navigating the DC-area real estate market

We've collected all our helpful guides for buying, selling and renting in and around Washington, DC in one place. Start browsing below!

First-Timer Primers

Intro guides for first-time home buyers

Unique Spaces

Awesome and unusual real estate from across the DC Metro

{kind=link}