UrbanTurf Puts Money Where Mouth Is, Part II

UrbanTurf Puts Money Where Mouth Is, Part II

✉️ Want to forward this article? Click here.

Two weeks ago, I posted that I recently took the plunge and purchased a two-bedroom condo in Logan Circle. That post outlined the specifics of the unit and my reasoning for buying. This second and final installment will cover everything from finding the unit to signing at the settlement table. If you have questions, post them in the comments section.

Front door of building

The Search

The properties that we feature on UrbanTurf are usually the result of hours of combing through homes on the DC area’s Multiple Listing Service (MLS). In early June, we came across a two-bedroom condo that we deemed worthy of our Deal of the Week feature.

I dropped by the unit toward the end of the first open house. The listing agent noted that 50 groups had come by in the first two hours, which based on the price and the scarcity of similar units on the market was probably pretty accurate.

It took two more trips back to the unit, a good deal of research about its value relative to condos of similar size in the neighborhood, and a long time pondering whether we wanted to put down the money that would be needed in order to make it happen.

To the last point, I won’t go into a great amount of detail about coming up with the down payment, but I will say that it came from wise investments made over the last ten years, contributions to a Roth IRA (that can be taken out without penalty) and other savings built up over the past few years.

Living Room

The Offer, The Negotiations and The Home Inspection

Our initial offer was $10,000 below the list price with a 3 percent credit to cover our closing costs. The counter offer was $5,000 below the list price and no credit to cover closing costs. We felt that another counter was pointless given that the unit was priced to sell, so after roughly 24 hours, both sides agreed to ratify the contract for $5,000 below the list price.

Knowing that we had agreed to the seller’s counter without any debate, our goal was to try to get a credit through the home inspection negotiations. The two-hour inspection revealed several items including a cracked back door, a non-functioning intercom, and a number of smaller issues that we felt should be fixed by the seller. The biggest issue was that none of the windows in the unit had “purchase”, i.e. a place to hold in order to open them.

The position we took with the seller regarding these repairs was to emphasize that they were unexpected costs. Rather than using the standard real estate form to present our case, we drafted a long narrative explaining the issues and asked the seller for a $7,000 credit, knowing that we would likely get half that amount. Five days and many emails later, the seller signed off on a $3,500 credit and also promised to make a number of smaller repairs worth about $750.

Kitchen

The Loan Approval

In the midst of all of this activity, we were collecting documentation for our loan approval. This was probably the most time consuming part of the process. It required collecting past W-2s, 1099s, federal tax returns, recent pay stubs and bank statements, and documentation of a homeowner’s insurance policy.

Because some of the funds for the down payment were coming from investment accounts, documentation was needed to show that the money had been transferred from the investment account to a checking account where all the money would be collected before it was wired to the title company. This part of the process made us realize how careful banks are being when approving loans. To make sure that the money was indeed coming from an investment account, and that we weren’t getting another loan to cover the down payment, the bank required an official letter stating the funds had been transferred. Even a copy of recent activity in the checking account showing that the money had been transferred from another account would not suffice. Our loan was eventually approved and a couple days before settlement, the bank issued cashier checks that looked like A-Rod’s per game salary.

The Big Day

On the day of settlement, we headed out to the title company in Bethesda and were soon seated across from the seller and listing agent. As a newbie, I found the proceedings a little awkward. I wanted to chat it up with the seller, talk about how excited I was to be buying the condo, etc. However, after a couple attempts, it became clear that she wanted to keep it all business, which was probably for the best in the end.

The closing proceedings are basically a chance to be reminded about everything from the interest rate you secured to how much you will be paying in condo fees. Also, it is a great chance to practice signing your name and initials.

The closing lasted around an hour and a half, and then we were officially homeowners.

I will happily answer questions about this process if readers have them, but reserve the right to keep certain information private. Just post them in the comments section and I will do my best to answer quickly.

This article originally published at http://dc.urbanturf.production.logicbrush.com/articles/blog/urbanturf_puts_money_where_mouth_is_part_ii/2397.

UrbanTurf Listings showcases the DC metro area's best properties available for sale.

Most Popular... This Week • Last 30 Days • Ever

Janeese Lewis George appears to have won Tuesday's Democratic mayoral primary, puttin... read »

This week’s Best New Listings includes a 100-year old bungalow in Hyattsville and a... read »

A new report shows that apartment rents in the DC region have fallen over the past ye... read »

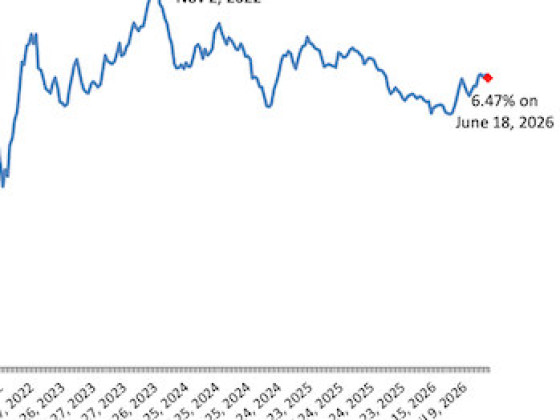

Freddie Mac reported Thursday that the 30-year fixed-rate mortgage averaged 6.47%, do... read »

Redbrick LMD has filed plans for a roughly 160-room hotel immediately adjacent to the... read »

DC Real Estate Guides

Short guides to navigating the DC-area real estate market

We've collected all our helpful guides for buying, selling and renting in and around Washington, DC in one place. Start browsing below!

First-Timer Primers

Intro guides for first-time home buyers

Unique Spaces

Awesome and unusual real estate from across the DC Metro

{kind=link}